Section 3 Market Performance Metrics

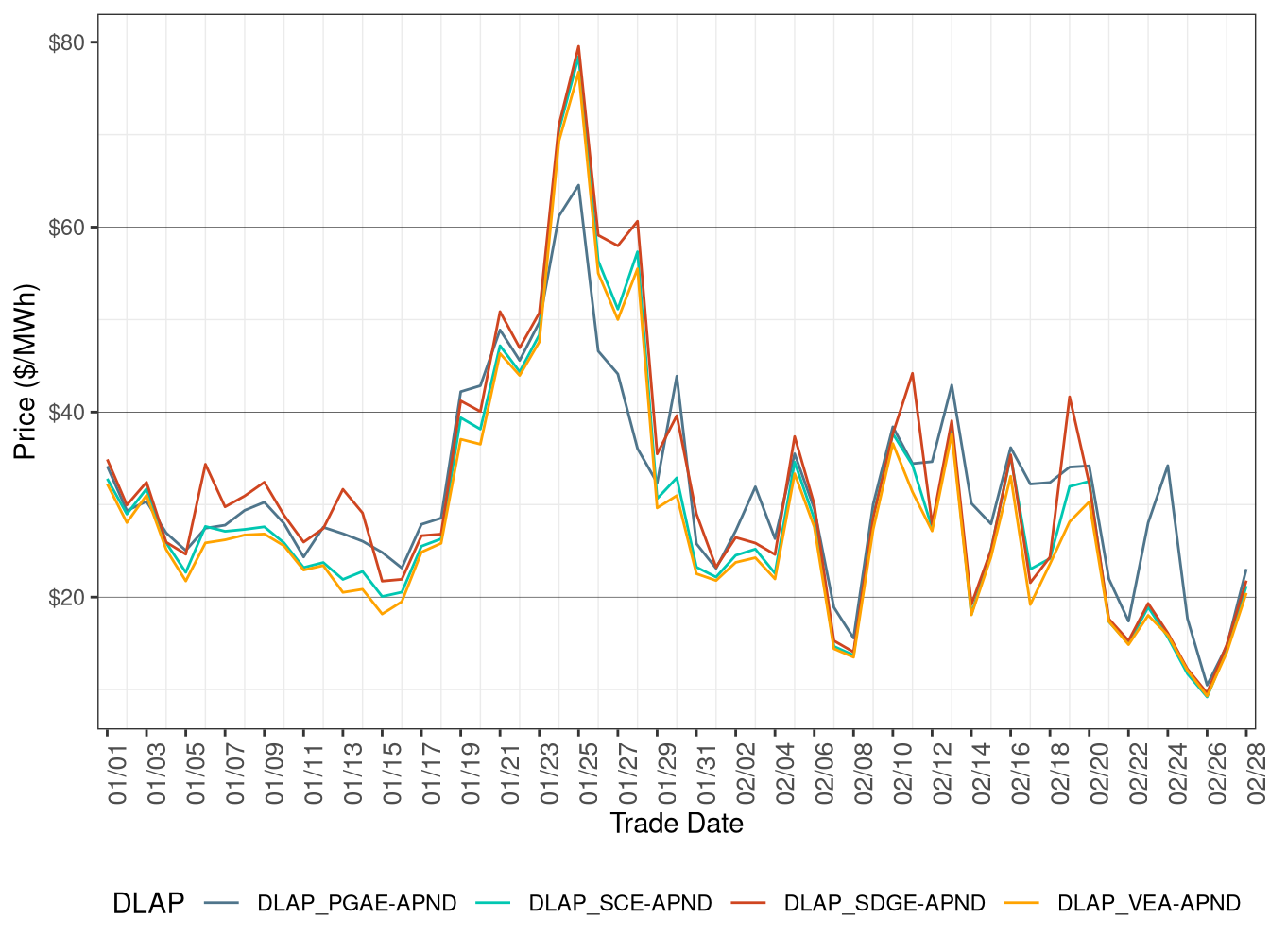

Day-Ahead Prices

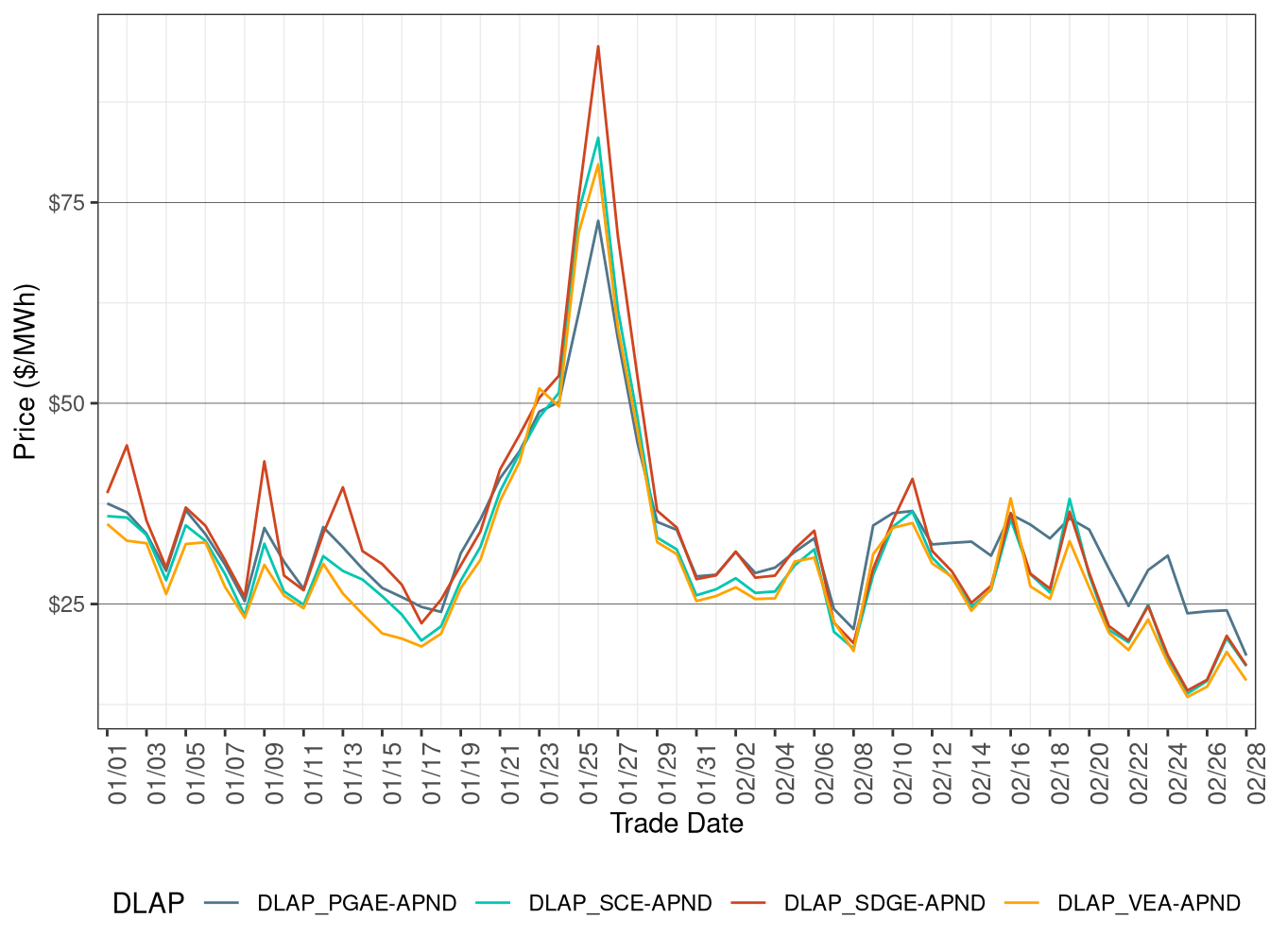

Figure 3.1 shows the daily simple average prices for all hours in IFM for each of the four default load-aggregation points (DLAP): PG&E, SCE, SDG&E, and VEA.

Average Day-Ahead DLAP prices in PGAE, SCE, SDGE, and VEA all decreased between from January 2026 to February 2026. This downward trend was likely driven by increased renewable generation, which suppressed Locational Marginal Prices (LMPs).

TABLE 3.1 below lists the binding constraints that resulted in relatively high or low DLAP prices on certain dates.

Figure 3.1: IFM (Day-Ahead) Simple Average DLAP Prices (All Hours)

| DLAP LMPs Affected | Dates | Transmission Constraint |

|---|---|---|

| PGAE | Feb 1 | PANOCHE-GATES-230kV line from HE 9 to HE 11 and on the MIDWAY-VINCENT-500kV line in HE 10 |

| PGAE | Feb 2 | TRCY PMP-TESLA D-230kV line from HE 9 to HE 16 |

| PGAE | Feb 3 | MOSSLD-LASAGUIL-230kV line from HE 9 to HE 16 |

| PGAE | Feb 4 | METCALF-METCALF-230 XFMR from HE 8 to HE 19 |

| PGAE | Feb 5-6 | METCALF-METCALF-230 XFMR from HE 8 to HE 11 |

| PGAE | Feb 7-8 | METCALF-METCALF-230 XFMR from HE 9 to HE 19 and on the PANOCHE-GATES-230kV line from HE 9 to HE 12 |

| PGAE; VEA | Feb 9-10 | METCALF-METCALF-230 XFMR from HE 8 to HE 16 |

| SDGE; VEA | Feb 11 | SUNCREST-SUNCREST-230 XFMR from HE 8 to HE 16 |

| PGAE | Feb 12 | LOSBANOS-PANOCHE-230kV line from HE 9 to HE 16 |

| PGAE; VEA | Feb 13 | MOSSLD-LASAGUIL-230kV line from HE 9 to HE 16 |

| PGAE | Feb 14 | PANOCHE-GATES-230kV line from HE 9 to HE 16 and on the MOSSLD-LASAGUIL-230kV line from HE 9 to HE 16 |

| PGAE; SDGE; VEA | Feb 15 | MOSSLD-LASAGUIL-230kV line from HE 9 to HE 15 and on the METCALF-METCALF-230 XFMR from HE 10 to HE 17 |

| VEA | Feb 16 | MORAGA-SN LNDRO-115kV line from HE 10 to HE 16 |

| PGAE | Feb 17-18 | METCALF-METCALF-230 XFMR from HE 9 to HE 16 and on the MIDWAY-VINCENT-500kV line from HE 9 to HE 16 |

| PGAE; SDGE; VEA; SCE | Feb 19 | LITEHIPE-MESA CAL-230kV line from HE 10 to HE 16 and on the DEVERS-DEVERS-500 XFMR from HE 8 to HE 22 |

| PGAE | Feb 20 | PANOCHE-GATES-230kV line from HE 9 to HE 16 and on the LOSBANOS-PANOCHE-230kV line from HE 9 to HE 16 |

| PGAE | Feb 21 | LOSBANOS-PANOCHE-230kV line from HE 9 to HE 16 and on the MIDWAY-VINCENT-500kV line from HE 9 to HE 16 |

| PGAE | Feb 22 | METCALF-METCALF-230 XFMR from HE 8 to HE 20 and on the LOSBANOS-PANOCHE-230kV line from HE 9 to HE 16 |

| PGAE | Feb 23 | DEVERS-DEVERS-500 XFMR from HE 8 to HE 24 and on the MOSSLD-LASAGUIL-230kV line from HE 9 to HE 16 |

| PGAE | Feb 24 | METCALF-METCALF-230 XFMR from HE 8 to HE 22 and on the LOSBANOS-PANOCHE-230kV line from HE 8 to HE 16 |

| PGAE | Feb 25 | PANOCHE-GATES-230kV line from HE 8 to HE 20 and on the METCALF-METCALF-230 XFMR from HE 8 to HE 21 |

| PGAE | Feb 26 | LOSBANOS-PANOCHE-230kV line from HE 8 to HE 17 and on the PANOCHE-GATES-230kV line from HE 8 to HE 17 |

| PGAE | Feb 27 | DEVERS-DEVERS-500 XFMR from HE 8 to HE 24 and on the LOSBANOS-PANOCHE-230kV line from HE 9 to HE 16 |

Real-Time Price

Figure 3.2 shows daily simple average prices for all four DLAPs (PG&E, SCE, SDG&E, and VEA) for all hours respectively in FMM.

Average FMM DLAP prices across PGAE, SCE, SDGE, and VEA decreased relative to the previous month.

TABLE 3.2 below lists the binding constraints that resulted in relatively high or low DLAP prices on certain dates.

Figure 3.2: FMM Simple Average DLAP Prices (All Hours)

| DLAP LMPs Affected | Dates | Transmission Constraint |

|---|---|---|

| PGAE | Feb 2 | MOSSLD-LASAGUIL-230kV line from HE 9 to HE 16 and on the TESLA-LOSBANOS-500kV line from HE 9 to HE 16 |

| PGAE | Feb 3 | TESLA-LOSBANOS-500kV line from HE 9 to HE 12 and on the MOSSLD-LASAGUIL-230kV line from HE 9 to HE 16 |

| PGAE; SDGE | Feb 4 | EL CAJON-LOSCOCHS-69kV line from HE 8 to HE 24 and on the MOSSLD-LASAGUIL-230kV line from HE 9 to HE 16 |

| SDGE | Feb 5 | PANOCHE-GATES-230kV line in HE 8 and on the MOSSLD-LASAGUIL-230kV line in HE 12 |

| PGAE | Feb 7 | MOSSLD-LASAGUIL-230kV line from HE 9 to HE 16 and on the PANOCHE-GATES-230kV line from HE 9 to HE 1 |

| PGAE | Feb 8 | PANOCHE-GATES-230kV line from HE 8 to HE 16 and on the GATES1-MIDWAY-500kV line in HE 9 |

| PGAE | Feb 9 | CAL CAPS-DEVERS-500kV line from HE 15 to HE 16 and on the EL CAJON-LOSCOCHS-69kV line from HE 17 to HE 19 |

| SDGE; VEA | Feb 11 | SUNCREST-SUNCREST-230 XFMR from HE 7 to HE 17 |

| PGAE | Feb 12 | MOSSLD-LASAGUIL-230kV line from HE 9 to HE 16 and on the PANOCHE-GATES-230kV line from HE 9 to HE 16 |

| PGAE | Feb 14 | MIDWAY-VINCENT-500kV line from HE 8 to HE 17 |

| PGAE | Feb 15 | PANOCHE-GATES-230kV line from HE 8 to HE 17 and on the LOSBANOS-PANOCHE-230kV line from HE 9 to HE 16 |

| PGAE; SDGE; SCE; VEA | Feb 17 | PANOCHE-GATES-230kV line from HE 8 to HE 19 and on the MIDWAY-VINCENT-500kV line from HE 9 to HE 17 |

| PGAE | Feb 18 | PANOCHE-GATES-230kV line from HE 8 to HE 17 and on the LOSBANOS-PANOCHE-230kV line from HE 9 to HE 16 |

| PGAE; SDGE; SCE; VEA | Feb 19 | OMS_19558673_TL23054_NG nomogram binding from HE 9 to HE 18 |

| PGAE | Feb 21-22 | MIDWAY-VINCENT-500kV line from HE 2 to HE 17 and on the MOSSLD-LASAGUIL-230kV line from HE 9 to HE 17 |

| PGAE | Feb 23 | LOSBANOS-PANOCHE-230kV line from HE 8 to HE 17 and on the MOSSLD-LASAGUIL-230kV line from HE 9 to HE 16 |

| PGAE | Feb 24-25 | PANOCHE-GATES-230kV line from HE 7 to HE 22 and on the LOSBANOS-PANOCHE-230kV line from HE 8 to HE 16 |

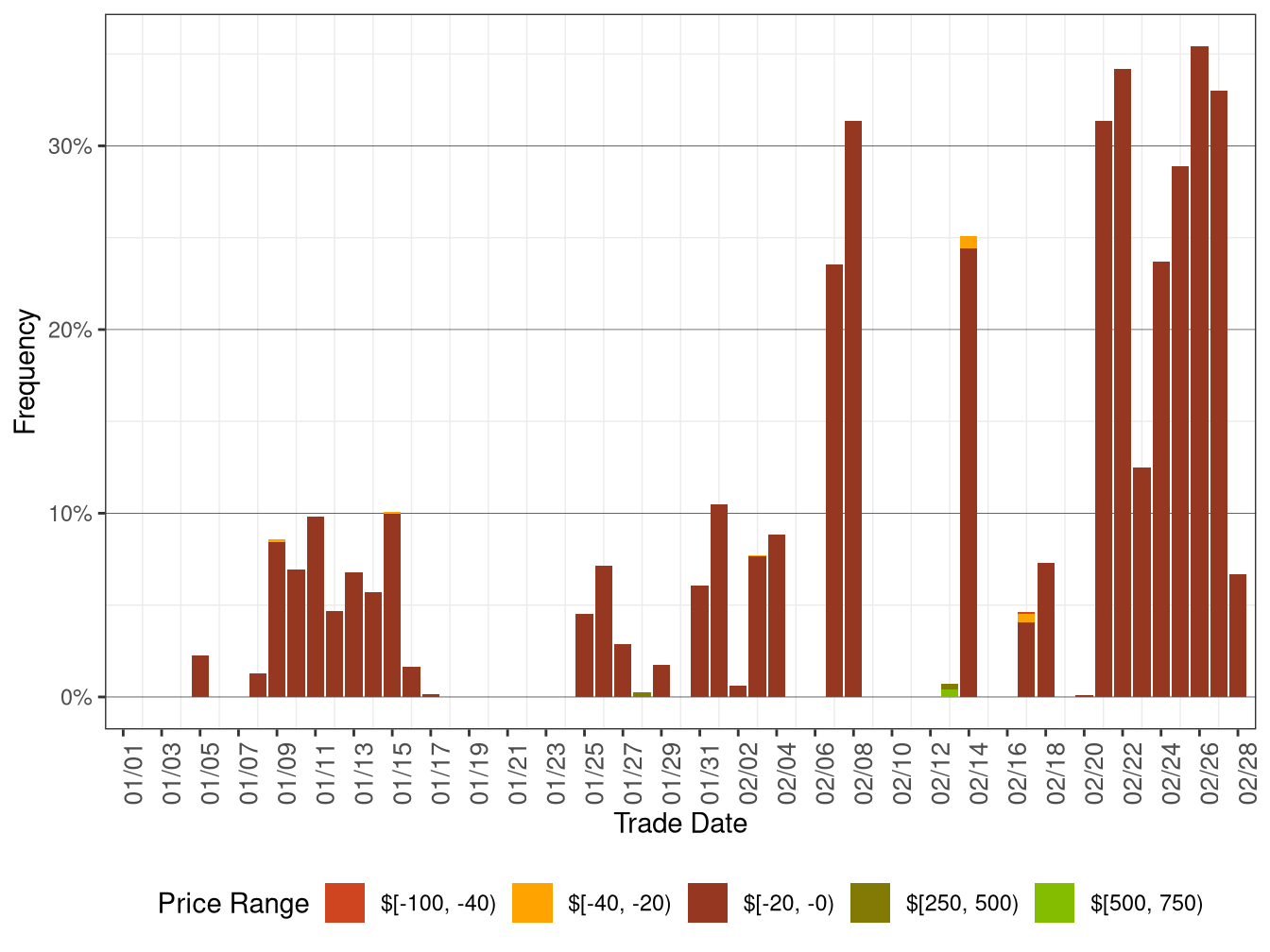

Figure 3.3 below shows the daily frequency of positive price spikes and negative prices by price range for the DLAPs in the FMM.

The cumulative frequency of prices in FMM above $250/MWh remained at 0 from January 2026 to February 2026, while the cumulative frequency of negative prices increased from 2.21 percent in January 2026 to 10.8 percent in February 2026.

Figure 3.3: Daily Frequency of FMM DLAP Positive Price Spikes and Negative Prices

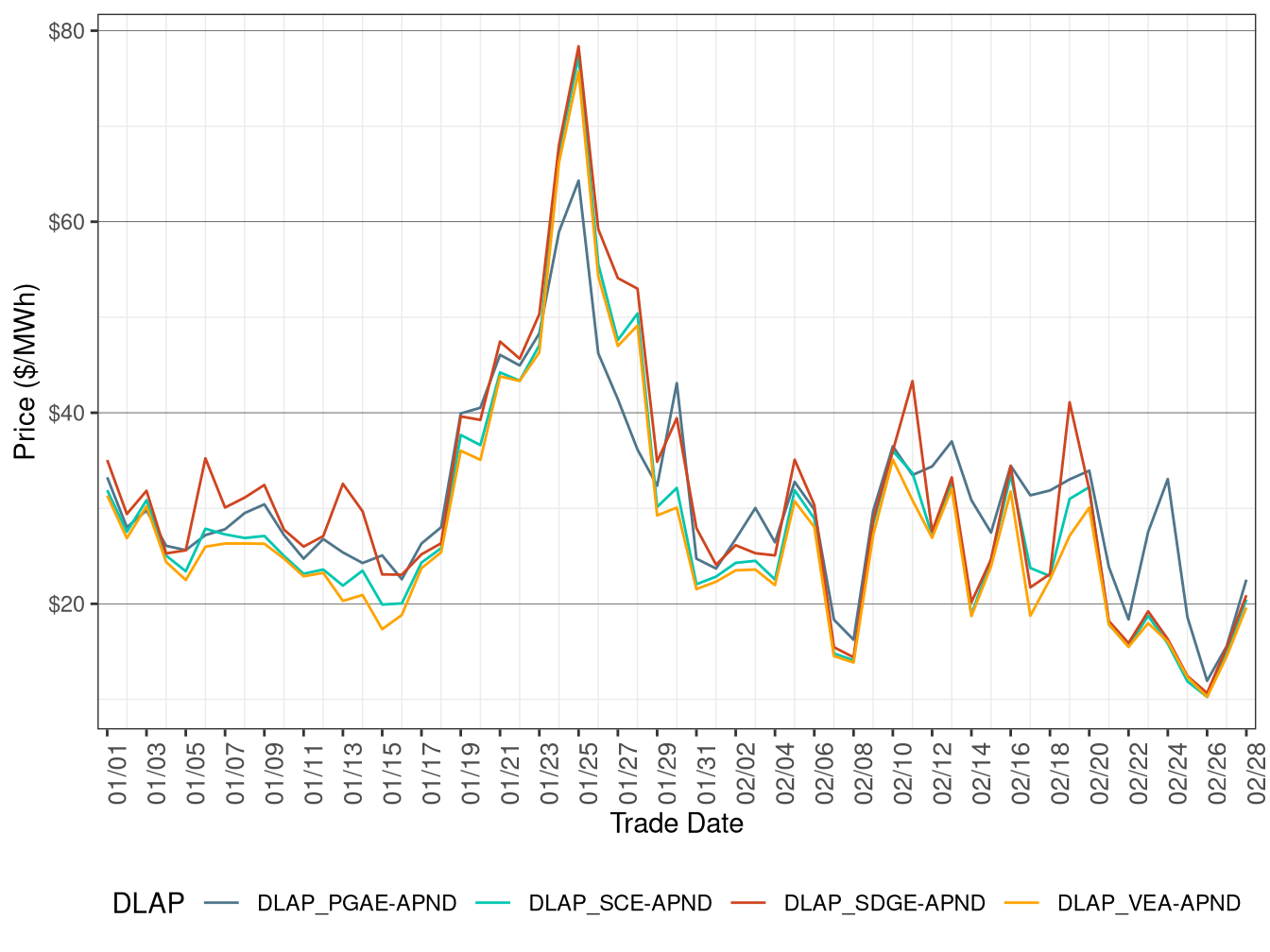

Figure 3.4 shows daily simple average prices for all the DLAPs (PG&E, SCE, SDG&E, and VEA) for all hours respectively in RTD.

Average RTD DLAP prices across PGAE, SCE, SDGE, and VEA decreased relative to the previous month.

TABLE 3.3 below lists the binding constraints that resulted in relatively high or low DLAP prices on certain dates.

Figure 3.4: RTD Simple Average DLAP Prices (All Hours)

| DLAP LMPs Affected | Dates | Transmission Constraint |

|---|---|---|

| PGAE | Feb 2 | MOSSLD-LASAGUIL-230kV line from HE 9 to HE 16 and on the TESLA-LOSBANOS-500kV line from HE 9 to HE 16 |

| PGAE | Feb 3 | GATES1-MIDWAY-500kV line from HE 9 to HE 11 and on the METCALF-METCALF-230 XFMR from HE 9 to HE 10 |

| PGAE; SDGE | Feb 4 | EL CAJON-LOSCOCHS-69kV line from HE 8 to HE 24 and on the PANOCHE-GATES-230kV line from HE 8 to HE 16 |

| PGAE | Feb 7 | MOSSLD-LASAGUIL-230kV line from HE 9 to HE 17 and on the TESLA-LOSBANOS-500kV line from HE 9 to HE 15 |

| PGAE | Feb 8 | PANOCHE-GATES-230kV line from HE 8 to HE 10 and on the GATES1-MIDWAY-500kV line from HE 9 to HE 16 |

| PGAE | Feb 10 | MIDWAY-VINCENT-500kV line in HE 24 |

| SDGE | Feb 11 | SUNCREST-SUNCREST-230 XFMR from HE 7 to HE 17 |

| PGAE | Feb 12 | MOSSLD-LASAGUIL-230kV line from HE 9 to HE 16 and on the PANOCHE-GATES-230kV line from HE 8 to HE 16 |

| PGAE | Feb 15 | PANOCHE-GATES-230kV line from HE 8 to HE 17 and on the LOSBANOS-PANOCHE-230kV line from HE 9 to HE 15 |

| PGAE; SDGE; SCE; VEA | Feb 16 | DEVERS-DEVERS-500 XFMR from HE 11 to HE 18 |

| PGAE; SDGE; SCE; VEA | Feb 17 | PANOCHE-GATES-230kV line from HE 8 to HE 19 and on the MIDWAY-VINCENT-500kV line from HE 9 to HE 17 |

| PGAE | Feb 18 | PANOCHE-GATES-230kV line from HE 8 to HE 17 and on the LOSBANOS-PANOCHE-230kV line from HE 9 to HE 16 |

| PGAE; SDGE; SCE; VEA | Feb 19 | OMS_19558673_TL23054_NG nomogram binding from HE 9 to HE 18 |

| PGAE | Feb 21-22 | MIDWAY-VINCENT-500kV line from HE 2 to HE 17 and on the MOSSLD-LASAGUIL-230kV line from HE 9 to HE 17 |

| PGAE | Feb 23 | LOSBANOS-PANOCHE-230kV line from HE 8 to HE 17 and on the MOSSLD-LASAGUIL-230kV line from HE 9 to HE 16 |

| PGAE | Feb 24-25 | PANOCHE-GATES-230kV line from HE 7 to HE 22 and on the LOSBANOS-PANOCHE-230kV line from HE 8 to HE 16 |

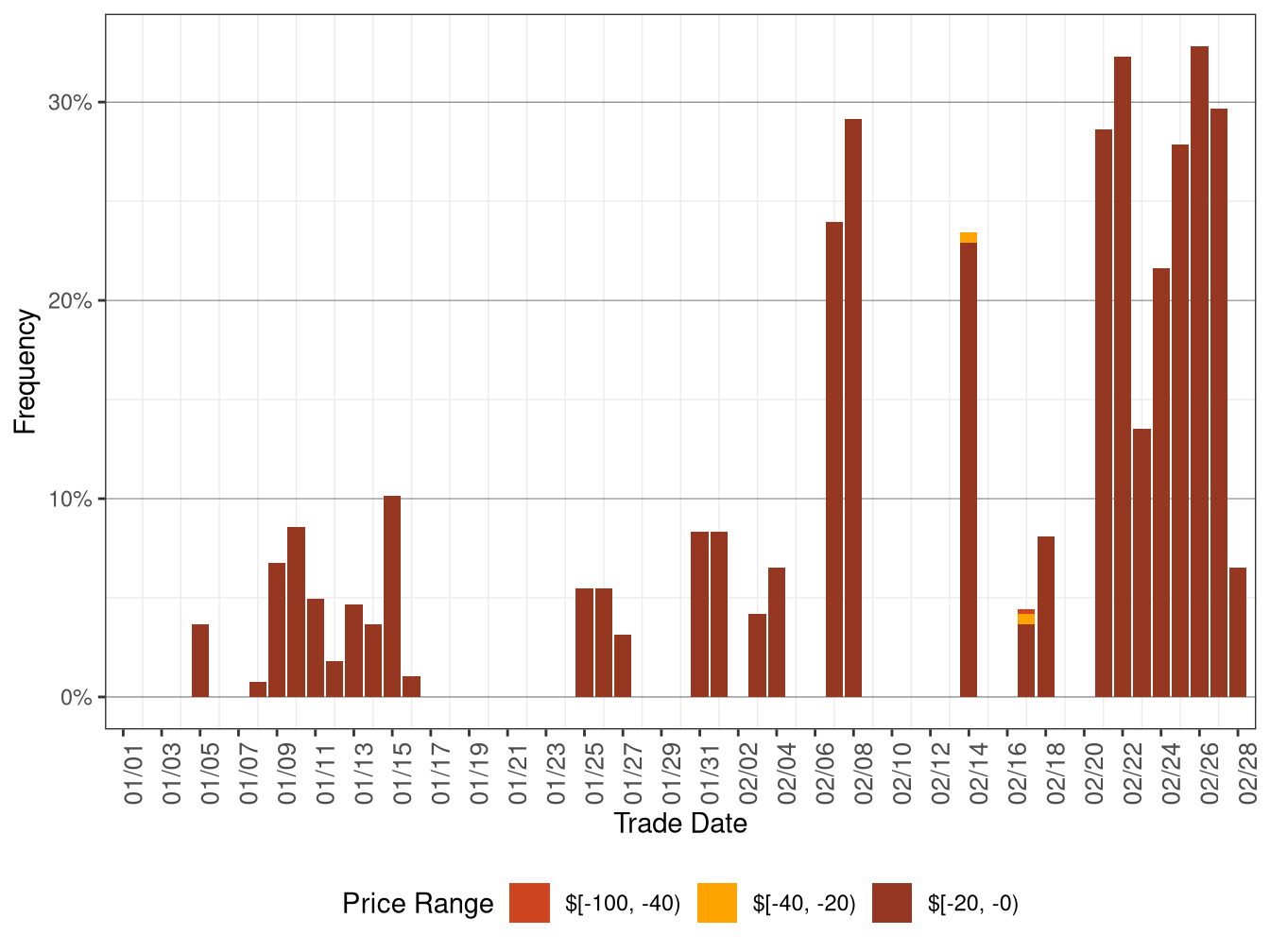

Figure 3.5 below shows the daily frequency of positive price spikes and negative prices by price range for the DLAPs in RTD.

The cumulative frequency of prices in RTD above $250/MWh increased from 0.01 percent in January 2026 to 0.025 percent in February 2026, while the cumulative frequency of negative prices increased from 2.59 percent in January 2026 to 11.6 percent in February 2026.

Figure 3.5: Daily Frequency of RTD DLAP Positive Price Spikes and Negative Prices