3 Market Performance Metrics

Day-Ahead Prices

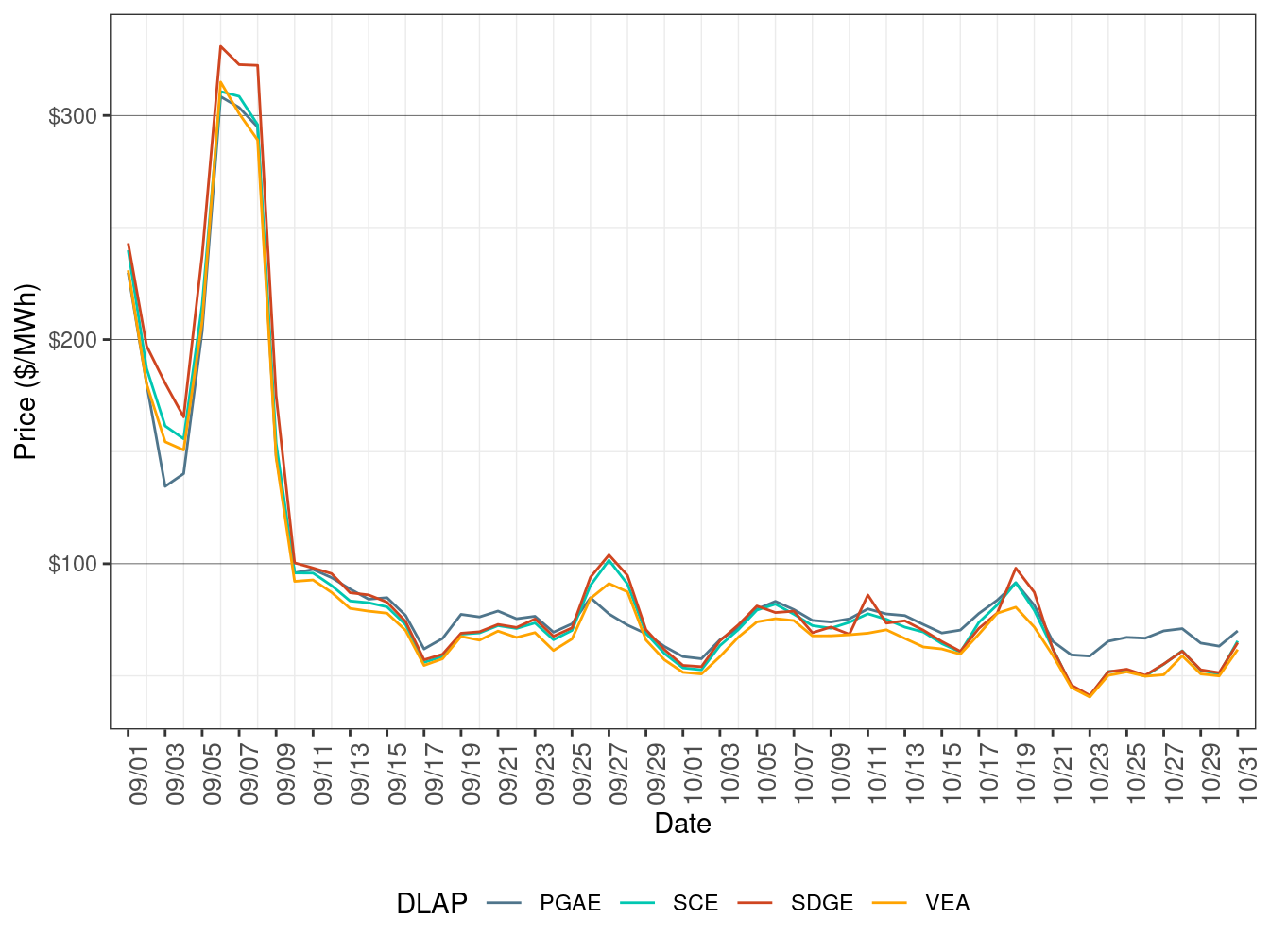

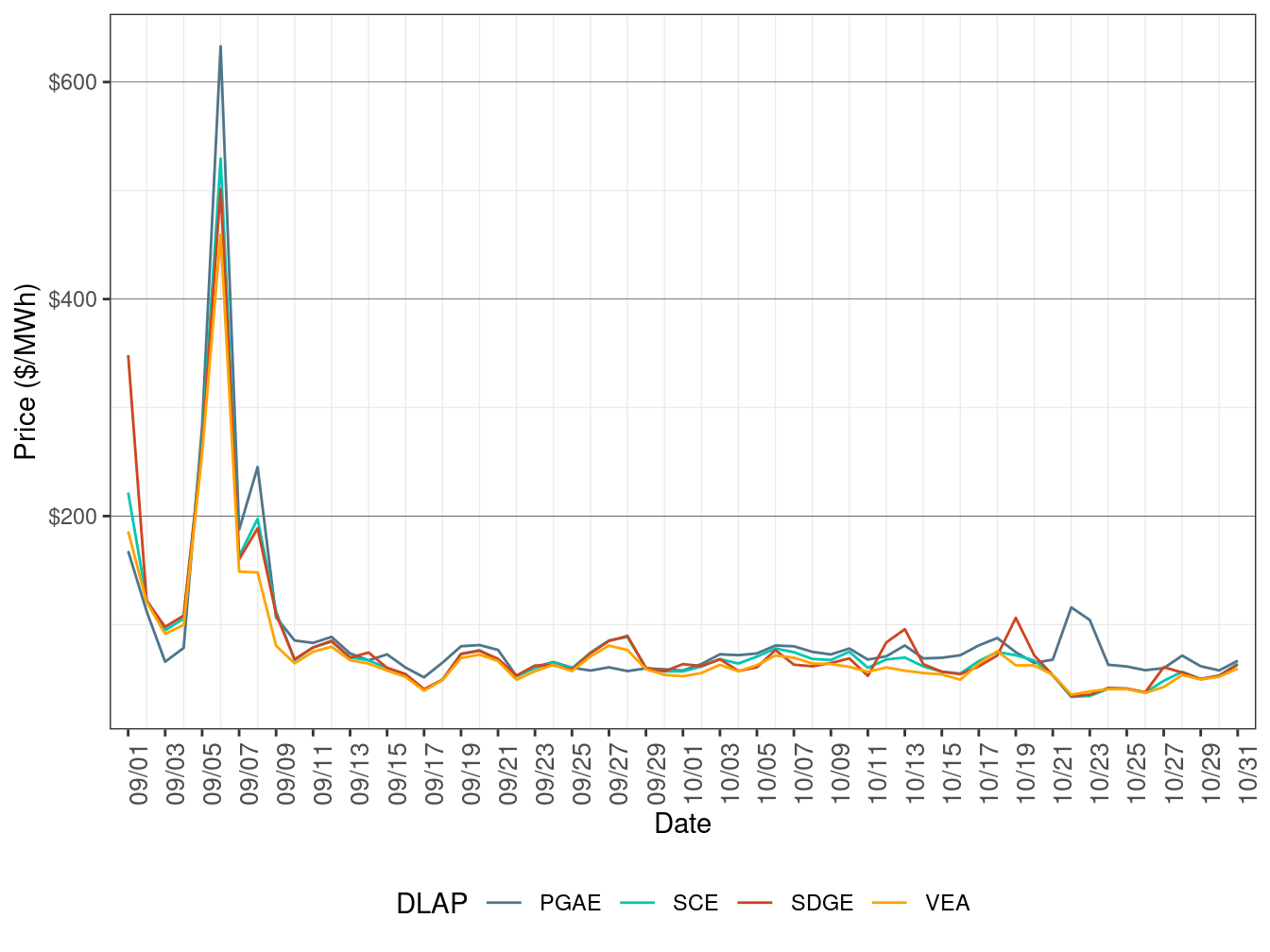

Figure 2 show the daily simple average load-aggregation points (LAP) prices for each of the four default LAPs (PG&E, SCE, SDG&E, and VEA) for all hours. Table 2 below lists the binding constraints along with the associated DLAP locations and the dates when the binding constraints resulted in relatively high or low DLAP prices.

Figure 2: Day-Ahead Simple Average LAP Prices (All Hours)

| DLAP | Dates | Transmission Constraint |

|---|---|---|

| PGAE | October 22, 24 | GATES-MIDWAY 230 kV line |

| PGAE | October 23 | GATES-MIDWAY 230 kV line, PANOCHE-GATES 230kV line |

| PGAE | October 25 | GATES-MIDWAY 230 kV line, GATES1-GATES 500 kV XFMR |

| PGAE | October 26-27 | GATES1-GATES 500 kV XFMR, Q0577SS-LOSBANOS 230 kV line, PANOCHE-GATES 230 kV line |

| PGAE | October 28-29, 31 | GATES1-GATES 500 kV XFMR, LOSBANOS-PANOCHE 230 kV line, PANOCHE-GATES 230 kV line |

| PGAE | October 30 | GATES-MIDWAY 230 kV line, LOSBANOS-PANOCHE 230 kV line |

Real-Time Price

Figure 3 show daily simple average LAP prices for all the default LAPs (PG&E, SCE, SDG&E, and VEA) for all hours respectively in FMM. Table 3 lists the binding constraints along with the associated DLAP locations and the dates when the binding constraints resulted in relatively high or low DLAP prices.

Figure 3: FMM Simple Average LAP Prices (All Hours)

| DLAP | Dates | Transmission Constraint |

|---|---|---|

| SDGE | October 12-13 | MIGUEL_BKs_MXFLW_NG |

| SDGE | October 19 | OMS_12018815-ML_BK80_NG |

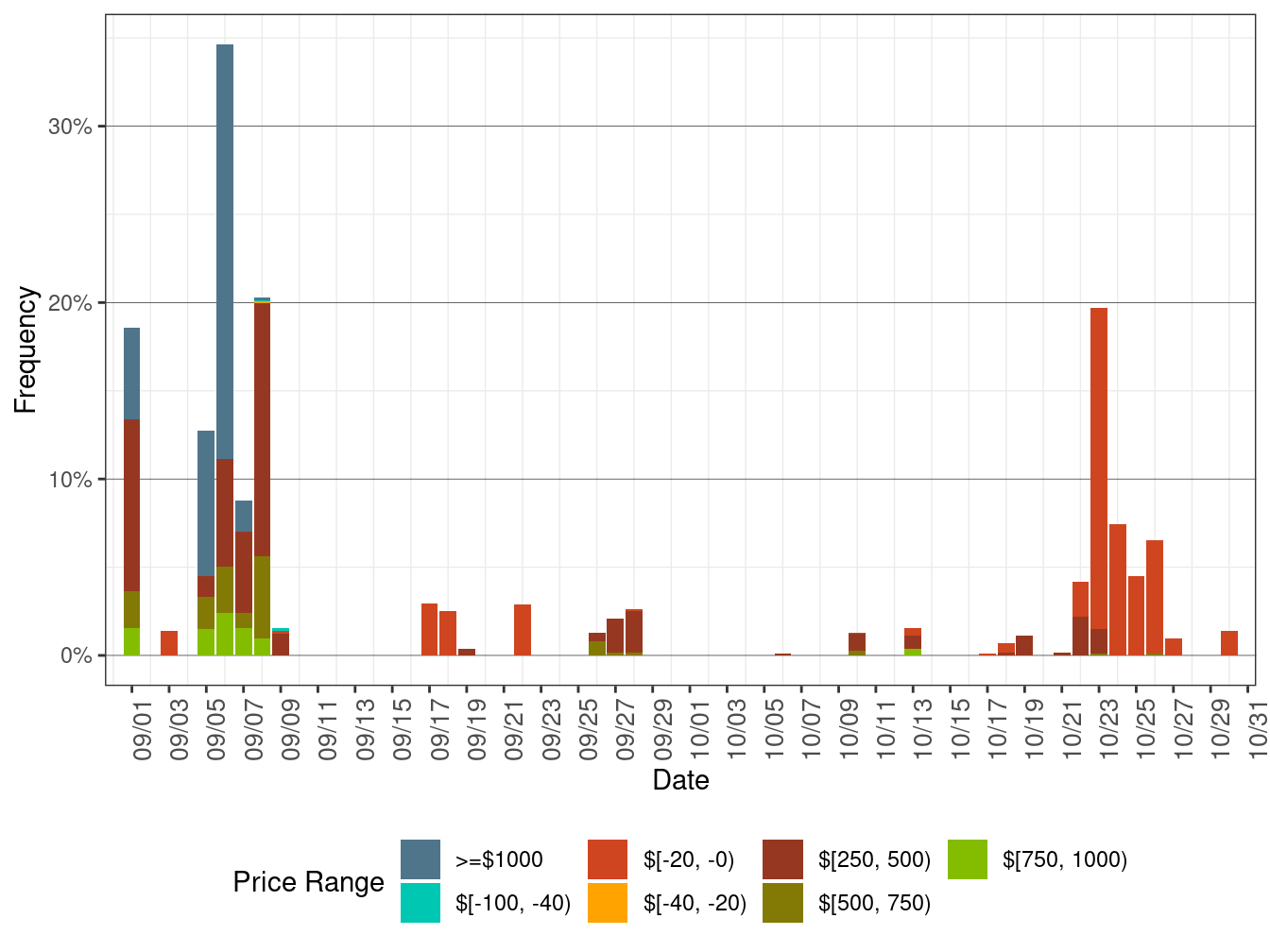

Figure 4 below shows the daily frequency of positive price spikes and negative prices by price range for the default LAPs in the FMM. The cumulative frequency of prices above $250/MWh dropped to 0.22 percent in October from 4.98 percent in September. The cumulative frequency of negative prices increased to 0.58 percent in October from 0.02 percent in September.

Figure 4: Daily Frequency of FMM LAP Positive Price Spikes and Negative Prices

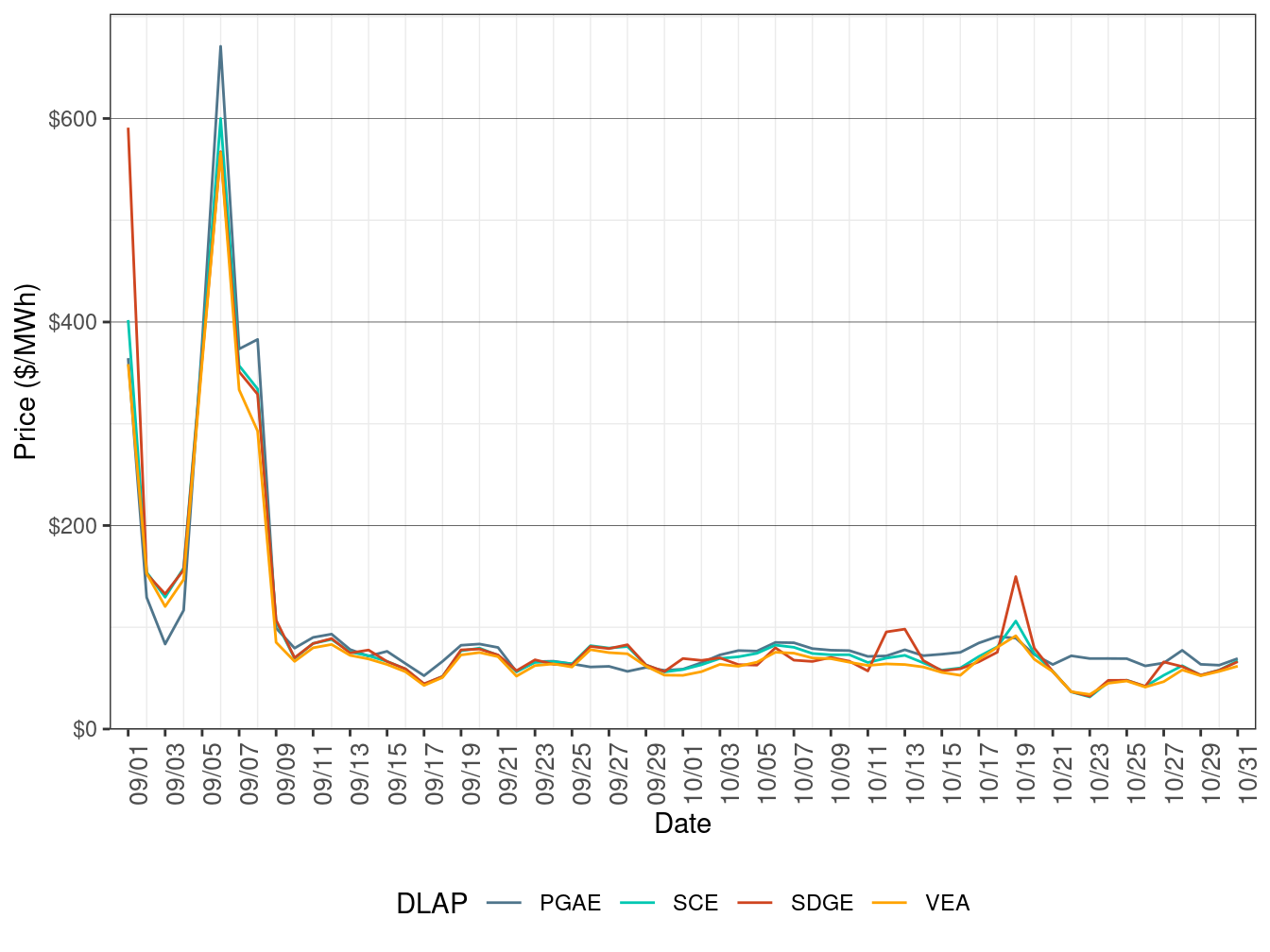

Figure 5 show daily simple average LAP prices for all the default LAPs (PG&E, SCE, SDG&E, and VEA) for all hours respectively in RTD. TABLE 4 lists the binding constraints along with the associated DLAP locations and the dates when the binding constraints resulted in relatively high or low DLAP prices.

Figure 5: RTD Simple Average LAP Prices (All Hours)

| DLAP | Dates | Transmission Constraint |

|---|---|---|

| SDGE | October 12-13 | MIGUEL_BKs_MXFLW_NG |

| SDGE | October 19 | OMS_12018815-ML_BK80_NG |

| PGAE | October 22 | GATES-MIDWAY 230 kV line, GATES1-GATES 500 kV XFMR |

| PGAE | October 23 | GATES1-GATES 500 kV XFMR, LOSBANOS-GATES1 500 kV line |

| PGAE | October 24-25 | GATES-MIDWAY 230 kV line, LOSBANOS-GATES1 500 kV line |

| PGAE | October 26 | LOSBANOS-GATES1 500 kV line, Q0577SS-LOSBANOS 230 kV line |

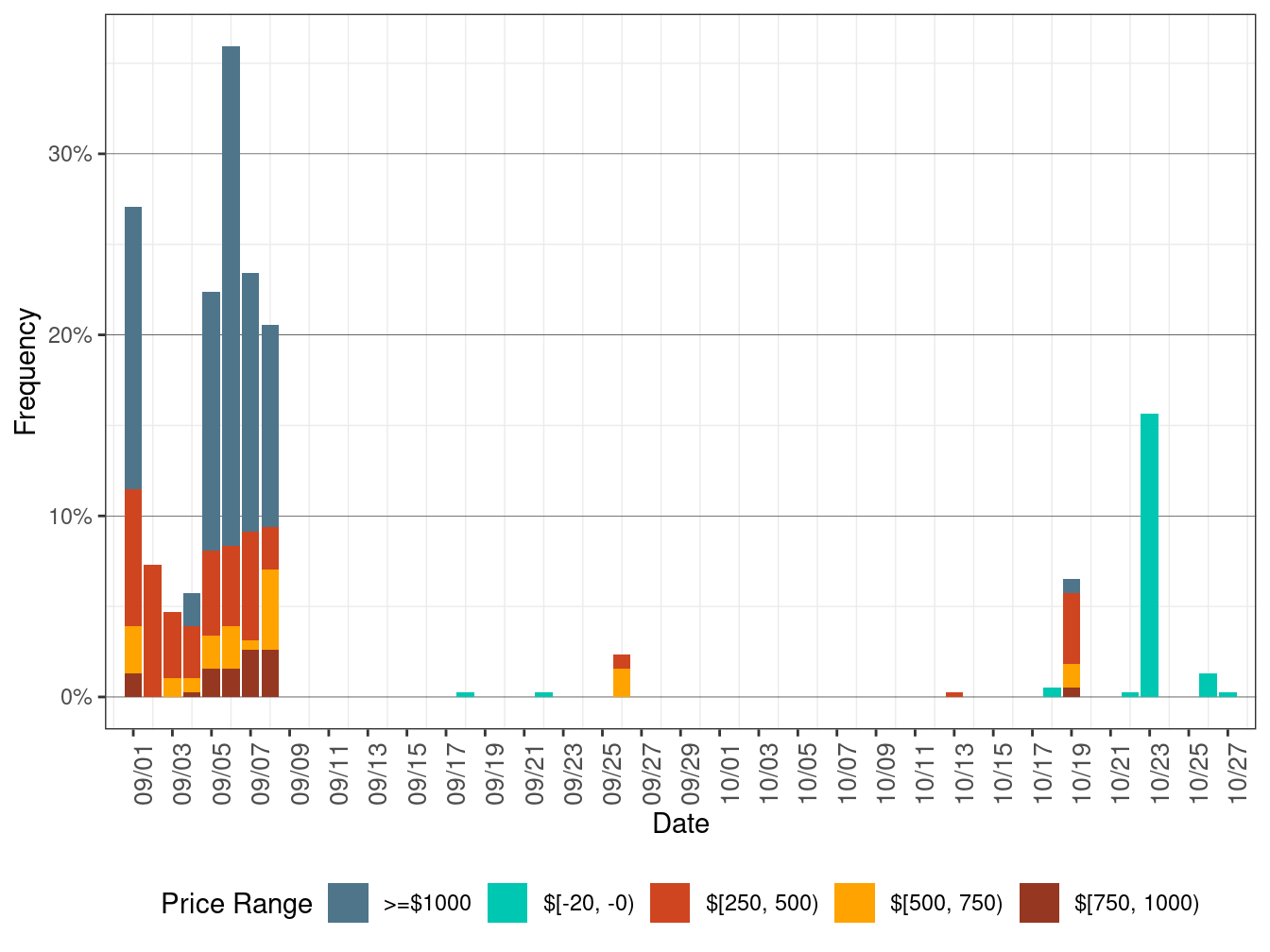

Figure 4 below shows the daily frequency of positive price spikes and negative prices by price range for the default LAPs in RTD. The cumulative frequency of prices above $250/MWh decreased to 0.25 percent in October from 3.41 percent in September. The cumulative frequency of negative prices increased to 1.36 percent in October from 0.34 percent in September.

Figure 6: Daily Frequency of RTD LAP Positive Price Spikes and Negative Prices